Sometimes people ask me if I “practice what I preach”. Though they usually say it differently. I hear things like, “Do you actually do this yourself?” or “Is this type of coaching only for people who have tons of money?” or “Is this only for people who have financial problems?”

So I thought I’d share an evening at home when I used my money coaching on myself. Picture this:

So I thought I’d share an evening at home when I used my money coaching on myself. Picture this:

It’s Thursday night and the Seahawks exhibition game is on in the background. I’m sitting on my couch with my laptop open, sipping on a cup of tea after dinner. My 14 year old son is half watching the game and half playing with his new I Phone- I think he’s checking his Facebook status every 2 minutes, texting, and watching YouTube. I’m eying the basket of laundry threatening out of the corner of my eye and texting my own friends about a date I went on last night.

I’m feeling a little stressed about money. So I know I need to look at where I am and see if there is anything I need to do differently this month.

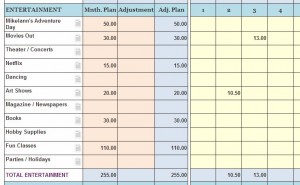

I open my wallet and pull out some receipts and then I log on to my MoneyMinderOnline subscription. (This is the financial tracking and spending plan tool I co-developed that people use to create a healthy relationship to money.) I enter what I spent over the last few days, taking note of a touchdown on the TV. I check my bank online to make sure I haven’t missed anything and I see an automatic payment that went through for a dating site I forgot to cancel (crap!), so I enter that too. And I make a quick note on my MoneyMinder action plan sheet to track down my log in and cancel that site.

Then I click to my august spending plan and look at what I planned to spend for the month, relative to what I actually did spend. Hmmm. I came back from a trip to Whistler last week, but it looks like I did a decent job of planning that. No real damage. Fabulous trip, too. I grab my phone and text a friend some Whistler pics.

Ah, but the issue is actually my dang eyesight. I spent two hours at the eye doctor unexpectedly today when I broke my eye glasses and emerged with….. progressive lenses…. I have been in denial about my changing eyesight. I’m in my fabulous forties and for some reason the print keeps getting smaller!

So I just dropped $600. Um, didn’t plan for that. Sigh.

Now my spending plan has my full attention. So I adjust my August plan for the glasses, and for some other things, like that dating site… I also see that I under-planned my son joining the high school football team. Cleats, sign up fees, equipment fees etc. Then I check to see what bills I have left to pay.

With a bigger sigh, I hit the summary button. The button says, “Does this plan work?” Well, gosh, no it doesn’t. If I don’t make any changes, it calmly informs me I will be negative in my account at the end of the month.

Another touchdown. It’s going to be a very good season.

I sip my tea and debate my life. I decide the way to handle the month is to wait on buying this new chair I’d been planning on buying for my living room. I can arrange this gorgeous throw I bought recently over the back of my current chair to give it a little life. And I’m also going to transfer in some money from my “periodic savings”. So I go online and quickly transfer the money and then I make the chair and savings adjustments on my august plan. Now I would end with enough money. Relief!

And when I thought about it, the glasses were on my annual plan- I just didn’t intend to do it this month. I decide that this weekend I’ll sit down and adjust my annual plan and look at the bigger picture. And I’ll update my needs and wants list. The eye glasses were definitely on the needs list. I will put the new chair on my wants list so I can prioritize for it.

For now, I am doing well. My stress is gone.

My son shows me a YouTube video he found on a rapper he likes. He’s trying to get me to see the light- “Rapping is cool, mom!”

Time to fold the laundry and pay closer attention to my Seahawks.

Want more help transforming your relationship to money? Check out all the eBooks, audios, and more robust products Mikelann has created. Are you ready to break free of the “money fog” and step into earning what you are worth? Are you are ready to get in touch with your emotions so you never feel out of control around money again? Are you ready to love your financial life? Let Mikelann help you get there. Free items are at the top of the page.

For some, there is an unconscious belief that money is bad- and people with money are greedy. Sound simple? Perhaps. But it is one of the many beliefs that can fuel underearning. Remember, underearning is when we consistently earn less than our potential. So what about you? In your heart of hearts, do you see money as good or bad?

For some, there is an unconscious belief that money is bad- and people with money are greedy. Sound simple? Perhaps. But it is one of the many beliefs that can fuel underearning. Remember, underearning is when we consistently earn less than our potential. So what about you? In your heart of hearts, do you see money as good or bad?

Also- heads up—I put together a HUGE audio program that will go on sale after my teleclass. It is a TWELVE AUDIO program on how to earn the money you truly deserve, and conquer underearning forever. “Unlock Your Earning Power”. It comes with 12 forty-minute audios and a 98 page companion workbook. I am not selling this through my own website (I took my store down), so your only opportunity to buy this program is through You Wealth Revolution Network. It is the result of many years of my work on earning issues and it may very well change your life. I’m extremely proud of it.

Also- heads up—I put together a HUGE audio program that will go on sale after my teleclass. It is a TWELVE AUDIO program on how to earn the money you truly deserve, and conquer underearning forever. “Unlock Your Earning Power”. It comes with 12 forty-minute audios and a 98 page companion workbook. I am not selling this through my own website (I took my store down), so your only opportunity to buy this program is through You Wealth Revolution Network. It is the result of many years of my work on earning issues and it may very well change your life. I’m extremely proud of it.

Last week I was the guest on the Chat With Women radio show. I think you’ll love the conversation we had about money. Listen to us discuss why people don’t talk about money, why people spend more when they visit a brand new store, how women spend differently than men, and how our money story impacts us. All that in 25 minutes. Here is the radio show link. It’s a 60 minute show. I am the guest for the first half.

Last week I was the guest on the Chat With Women radio show. I think you’ll love the conversation we had about money. Listen to us discuss why people don’t talk about money, why people spend more when they visit a brand new store, how women spend differently than men, and how our money story impacts us. All that in 25 minutes. Here is the radio show link. It’s a 60 minute show. I am the guest for the first half.

1. Set a timer. After you have shopped for 90 minutes, you tend to go into a zone- and you spend more mindlessly. You zone out. Malls encourage this by hiding the passage of time. They don’t post clocks or have a lot of windows. This way you don’t know how much time has passed. So simply set a timer on your phone for 90 minutes. When it goes off, sit down and have a cup of tea. You don’t have to go home. Just take five minutes to relax and assess where you are, what you’ve purchased and what else you want to do.

1. Set a timer. After you have shopped for 90 minutes, you tend to go into a zone- and you spend more mindlessly. You zone out. Malls encourage this by hiding the passage of time. They don’t post clocks or have a lot of windows. This way you don’t know how much time has passed. So simply set a timer on your phone for 90 minutes. When it goes off, sit down and have a cup of tea. You don’t have to go home. Just take five minutes to relax and assess where you are, what you’ve purchased and what else you want to do.

I know countless savvy women who don’t see themselves as “strugglers”, but they don’t see themselves as financially abundant either. They make decent money, as relative as that is. And they are really frustrated. Why? Because they know in their minds and their hearts that they could make more. They know, at some level, that they are earning less than their true potential.

I know countless savvy women who don’t see themselves as “strugglers”, but they don’t see themselves as financially abundant either. They make decent money, as relative as that is. And they are really frustrated. Why? Because they know in their minds and their hearts that they could make more. They know, at some level, that they are earning less than their true potential.

I build my mortgage payment into my monthly spending plan and on-going maintenance and improvements are part of my annual spending plan. (Before I bought my house I had a category called “house down payment” in my spending plan, where I saved money each month in preparation to buy my sweet home.)

I build my mortgage payment into my monthly spending plan and on-going maintenance and improvements are part of my annual spending plan. (Before I bought my house I had a category called “house down payment” in my spending plan, where I saved money each month in preparation to buy my sweet home.)